Strait of Hormuz Crisis: How the Iran War Is Reshaping Global Oil Markets and the World Economy

With 20% of global oil supply disrupted, LNG plants shuttered, and flights grounded across the Gulf, the economic shockwaves of Operation Epic Fury are being felt from Wall Street to New Delhi.

The military campaign against Iran was always going to have economic consequences far beyond the battlefield. But the speed and severity of the disruption has exceeded even the most aggressive forecasts. Within days of the first strikes on February 28, the conflict transformed from a geopolitical risk premium into a real-time supply crisis — one that is now repricing energy, shipping, insurance, aviation, and financial risk simultaneously across the global economy.

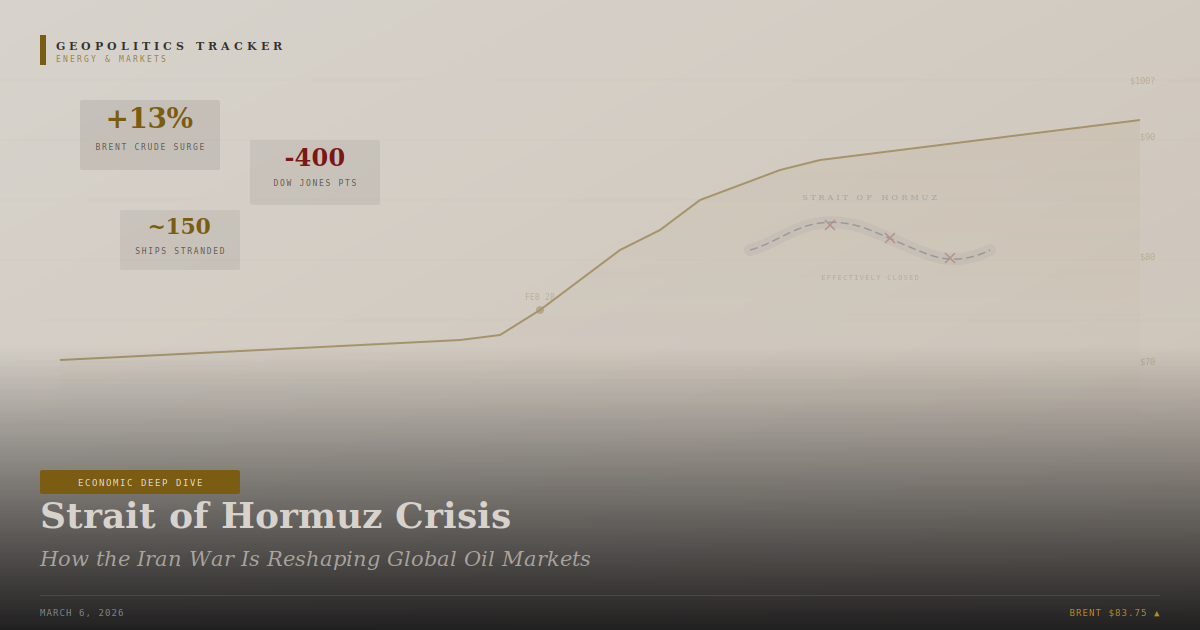

| $83.75 | +13% | 20% | ~150 |

|---|---|---|---|

| Brent Crude / Barrel | Oil Price Surge (Peak) | Global Oil via Hormuz | Ships Stranded |

The Strait of Hormuz: From Risk Premium to Actual Disruption

The Strait of Hormuz has always been the single most important chokepoint in global energy. Approximately 20 million barrels of oil and petroleum products pass through the narrow waterway between Iran and Oman every day — roughly one-fifth of all global petroleum consumption and more than a quarter of seaborne oil trade. It also carries about 20% of the world's liquefied natural gas.

When the IRGC declared the Strait closed on March 3 and warned that any vessel attempting passage would be targeted, the threat was not entirely empty. At least five tankers have been damaged, two crew members killed, and approximately 150 ships remain stranded in surrounding waters, as reported by Al Jazeera. While some vessel traffic technically continues, the withdrawal of commercial operators, major oil companies, and insurers has created what energy analysts at Kpler describe as a de facto closure for most global shipping, with insurance premiums at six-year highs making transit economically unviable.

The Stimson Center's analysis frames the Strait not merely as a tactical lever, but as a transmission belt between regional war and the global economy. The question confronting markets, the analysis argues, is whether the war has pushed the Strait from a routine geopolitical premium into a genuine supply disruption with broader consequences for inflation, currencies, and emerging markets.

Oil, Gas, and the Cascading Supply Shock

The numbers tell a stark story. Brent crude surged 10–13% from approximately $70 to over $80 per barrel within days of the strikes beginning, according to compiled economic data. By March 6, Brent stood at $83.75 per barrel. Analysts cited by Bloomberg and other outlets have warned that prices could reach $100 if disruptions persist, potentially adding 0.8 percentage points to global inflation.

The gas market has been hit even harder in percentage terms. QatarEnergy halted activity at the world's largest LNG export facility — Ras Laffan Industrial City — after it was targeted in an Iranian drone attack, as Bloomberg reported. European natural gas prices nearly doubled following the shutdown of Qatari facilities, raising fears of energy security crises in countries that had only recently rebuilt supply chains after the 2022 disruptions caused by the Russia-Ukraine war.

Hormuz is not merely a tactical lever Iran can threaten or the United States can defend. It is a transmission belt between regional war and the global economy.

— Stimson Center analysis by Umud Shokri, March 3, 2026

Who Gets Hurt: A Global Impact Map

Bloomberg Economics framed the core problem clearly: for Europe, sustained higher energy prices push the economy to the brink of recession; for the United States, they put the Federal Reserve in an impossible position between war-driven inflation and presidential demands for rate cuts.

Asia's oil-importing economies face the most direct impact. China, India, Japan, and South Korea collectively account for 75% of oil exports and 59% of LNG exports from the Gulf region. India, which relies heavily on Gulf countries for its oil imports, is monitoring the situation as a significant drawdown in reserves is expected to drive up domestic inflation, according to compiled economic impact reporting. Gold prices in India swung dramatically after the disruption of shipments through Dubai, the usual transit hub.

For Gulf economies themselves, the situation is paradoxical. While higher oil prices theoretically boost revenue, the physical disruption — grounded flights, shuttered LNG plants, damaged infrastructure — is devastating. A Wirtschaftswoche analysis concluded that a prolonged conflict would be catastrophic for economies like Qatar and the UAE that depend on stable trade routes and tourism. About 10% of the world's container ships are caught up in broader shipping disruptions, and cargo is starting to pile up at ports across Europe and Asia, according to the CEO of container carrier Ocean Network Express.

The landlocked countries of Central Asia face a less obvious but potentially severe blow. These nations depend on Iranian ports as trade corridors to reach Europe and South Asia. With those routes disrupted, they face increased dependence on northern corridors through Russia — an uncomfortable position that undermines years of diversification efforts.

Markets, Safe Havens, and the Defence Trade

Financial markets have followed a familiar wartime pattern — with important exceptions. The Dow Jones fell over 400 points on March 2 as the reality of the conflict set in. Investors moved toward traditional safe-haven assets: gold, the Japanese yen, and the Swiss franc all saw increased demand.

Morgan Stanley's analysis noted that markets have historically posted gains during wartime, including double-digit increases during both Gulf Wars in the three to six months following onset, led by the defence sector. The firm advised investors to consider increasing exposure to defence, security, aerospace, and industrial resilience themes — areas where government spending can drive multi-year demand. But it also cautioned that geopolitical risk is becoming a persistent feature of the investment landscape rather than an episodic one.

Oxford Economics estimated that inbound arrivals to the Middle East could decline 11–27% year-on-year as tourism collapses, further compounding economic pain for Gulf states that have invested heavily in diversifying beyond oil.

The Administration's Economic Pain Threshold

There is a critical political dimension to the economic fallout. The Trump administration has publicly stated it is not concerned about oil prices. But as Kpler's analysis notes, sustained Brent above $90 per barrel for one to two weeks would represent a meaningful headwind to domestic economic messaging — the same kind of pressure that prompted rapid tariff adjustments earlier this year. If that threshold is breached, a policy recalibration on the military campaign itself becomes more likely.

Meanwhile, the conflict adds yet another layer of uncertainty to a global economy already grappling with Trump's tariff policies, fragile European recovery, and slowing Chinese demand. The combined effect of trade war and actual war on energy prices creates what economists describe as a compounding risk environment that is exceptionally difficult for central banks to navigate.

Whether the economic damage proves temporary or structural depends entirely on how long the conflict lasts and whether the Strait of Hormuz can be effectively reopened. OPEC+ retains approximately 3.5 million barrels per day of spare capacity, concentrated in Saudi Arabia and the UAE. However, as Kpler notes, a significant portion of that capacity cannot reach global markets if the Strait itself remains inaccessible. Alternative pipeline routes exist but cannot fully offset a prolonged closure.

Sources & Further Reading

- Bloomberg — Oil & Hormuz Disruption

- Bloomberg Economics — Global Recovery at Risk

- Kpler — Strait of Hormuz Analysis

- Stimson Center — Economic Shockwaves

- Morgan Stanley — Iran Oil & Inflation

- Oxford Economics — Initial Take

- Al Jazeera — Oil Crisis Analysis

- Wikipedia — Economic Impact of the 2026 Iran War